Sometimes we at the Foundation have to save our government from accidentally shooting itself in the foot.

In our current legislative session, the Hawaii Department of Transportation (HIDOT) introduced Senate Bill 1473, Relating to Central Services Assessment. HIDOT’s work is largely paid for by special funds, namely the Highway Fund, the Airport Revenue Fund, and the Harbor Special Fund. But, as we explained in a series we published in 2017 called “The Grand Skim of Things,” most of the special funds, including the three Department of Transportation funds just mentioned, need to pay a 5% “Central Services Assessment” to the General Fund annually to compensate the rest of the government for shared services.

The amount skimmed from the Department of Transportation’s three funds was not chicken feed by any means. According to a report prepared at the end of 2024, the Highway Fund got hit for $11.7 million, the Harbor fund paid $8.6 million, but the Airport fund got stung the hardest for $18.1 million.

Apparently, the good folks at the Department of Transportation were so annoyed by this skim that they introduced the bill. The bill chops the skim down to a blank amount, or 2.5% of the fund, whichever is less. The blank amount (to be filled in by a later committee) would be adjusted for inflation in later years.

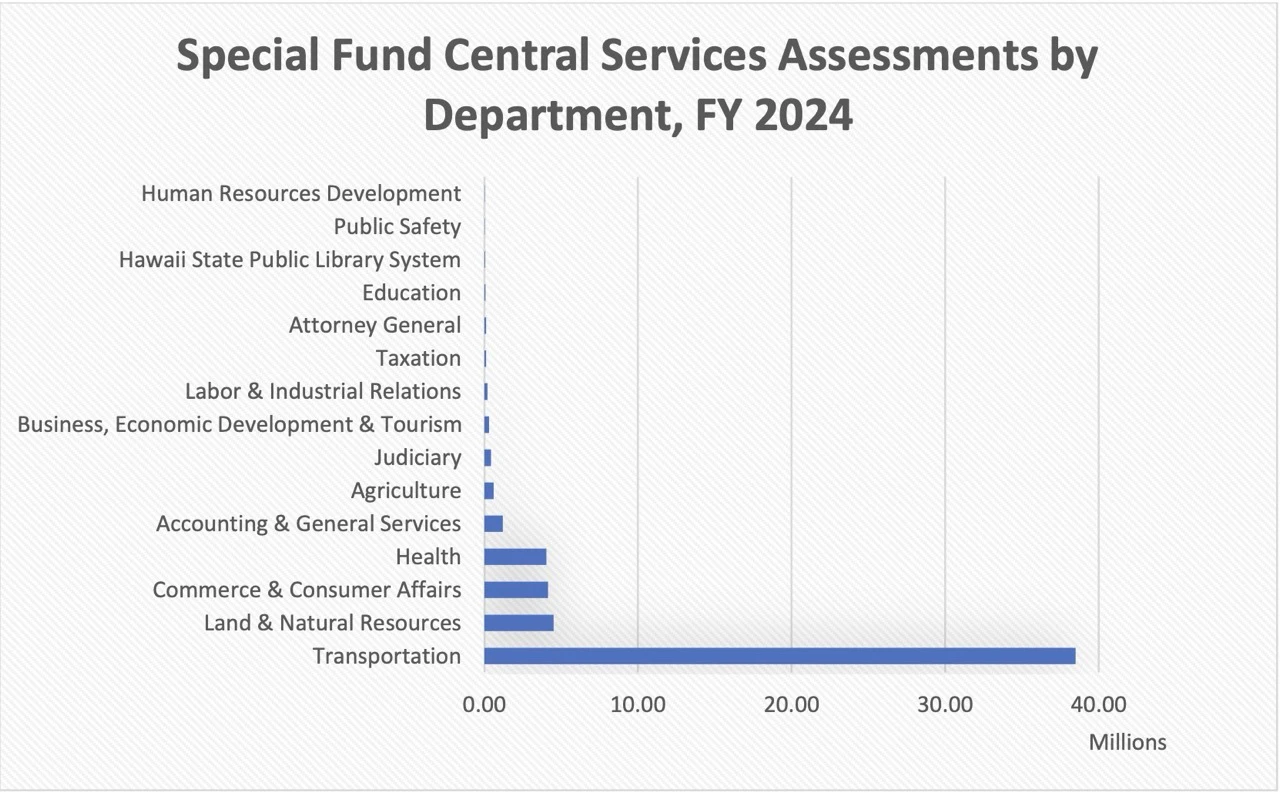

In testimony before the House Finance Committee, HIDOT complained that its central services assessment contributions “have constituted a majority of the funds contributed by departments to defray the cost of central government services—a majority both in percentage and on a per-employee basis.” HIDOT is certainly bearing much of the burden, as this chart shows, because some of the larger departments either are not special funded, have one of 30+ exemptions (see HRS 36-27) from the assessment, or simply refuse to pay it (Department of Hawaiian Home Lands):

Source: Department of Budget and Finance

HIDOT, however, forgot to take one wrinkle into account. There is a federal law prohibiting any tax, fee, or charge first taking effect after 1994 exclusively upon a business located at an airport unless the tax, fee, or charge is wholly utilized for airport or aeronautical purposes. 49 U.S.C. § 40116(d)(2)(A)(iv). The central services assessment against the Airport Fund under HRS § 36-28.5 is now allowed because the statute was last amended in 1970 and is thus grandfathered. So, the wrinkle is that if the statute is amended, it becomes a fee or charge taking effect after 1994, and a central expense assessment of any amount against the airport fund would not be allowed because that money would not be used solely for airport or aeronautical purposes.

We mentioned this to House Finance Committee, sort of by accident because the bill was not initially on our radar.

After thinking about it over the weekend, the Committee killed the bill.

Which is a good thing, in a way, because if the special funds aren’t contributing this $55 million to our governmental expenses, then the government would be looking to get that money from somewhere else. From us, perhaps.

Tom Yamachika is president of the Tax Foundation of Hawaiʻi. Reprinted with permission.